No products in the cart.

Curacao Business

Businesses Going Forward Towards a New Normal

03

Jul

Jul

March 31, 2020

Businesses going forward towards a new normal

The COVID-19 outbreak that started in China last year has now spread around the globe, also affecting the Dutch Caribbean islands. Although the number of infected citizens and associated deaths is still below the European and American levels, our health authorities and government officials are addressing the threat with maximum care.

Temporary precautionary measures coupled with the adverse impact of the virus internationally are having a profound negative effect on our economy and local businesses, especially the ones that are directly dependent on tourism. In addition, the closure of all non-vital companies is having a severe and disrupting effect in our small, inter-connected economy. Over the next few months, our business leaders will face the challenge of keeping their companies on track, while first and foremost guaranteeing the health and safety of their workers and communities.

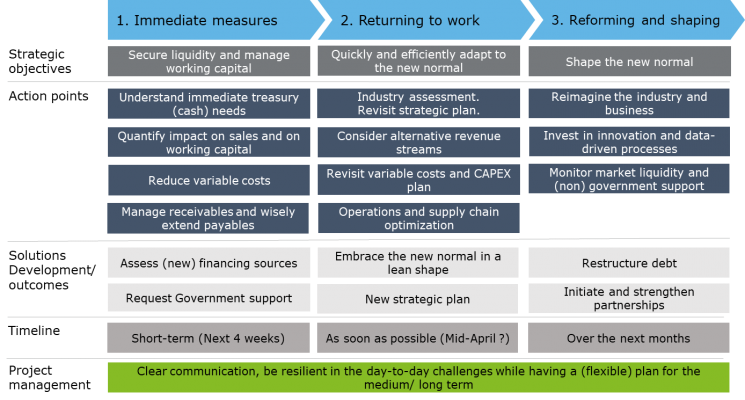

Immediate measures

Top priority for the business community is to ensure sufficient liquidity and acceptable levels of working capital. The starting point should be a quick scan of businesses’ cash as well as its inventory, accounts receivable and accounts payable positions (broadly defined as working capital). After this first assessment, businesses should quantify the negative impact that the decline in sales and supply chain inefficiencies may have on their financial position by creating different scenarios with varying associated probability levels.

Meanwhile, business leaders may benefit from immediately reducing certain variable expenses while maximizing its account receivables collection. If needed, companies may try to negotiate their payables conditions with their suppliers, however with caution to prevent a transfer of the liquidity problem further in the supply chain which can lead to future late deliveries as well as added strain to the commercial relationship.

Even after performing these steps successfully, additional funding may still be required to bring liquidity to acceptable levels. Businesses should engage with their existing financing partners and understand whether the existing financing options – overdrafts, credit lines, guarantee letters – are still available and what terms and conditions would apply to new, bigger facilities.

When trying to secure financial support, it is key to put up a credible case by getting the facts right and delivering high-quality, relevant information. This will increase the chance of obtaining the required financing at better terms and conditions. The same applies for the local governments support measures that are currently being announced and which details will follow shortly.

Returning to work

While there is still no expected date for resumption of normal operations, the business community should urgently start to imagine and plan for what could be referred to as “new normal” times.

When resuming operations, businesses should try to grasp the new industry dynamics and evaluate whether their strategic plans and operations are still valid. Companies may consider alternative revenue streams and different ways of doing business. They will also have the opportunity to revisit their variable cost structure and change their investment plans to reflect new strategic objectives and available funds.

On a more operational level, the supply chains will most likely need to be optimized by focusing on a more efficient planning of the workforce and by using an agile production scheduling. Unnecessary production processes should be eliminated or re-processed to fit the specific demand of the – new – business. This includes alternative inbound and outbound logistics channels, the latter being particularly relevant for our island quick recovery and positioning. A clear visibility of materials is key and so inventories should be reviewed by assessing the resulting production frequency and associated optimal stock levels. IT systems need to be aligned to provide clear data and guidelines on which decisions can be made.

Following this overall operational assessment, new strategic plans will lead to new ways of doing business going forward. To successfully make this transition, businesses should maintain stakeholder engagement while constantly adapting to new developments by using lean processes and innovative approaches.

Reforming and shaping

The next few months will be extremely hard for the majority of businesses and their customers. Yet, times of disruption present opportunities for certain businesses to become leaders and shapers of their industries.

Innovation and agility should be key, since businesses that are able to quickly adapt and take data-based decisions will be better positioned to succeed. Efficient cash management processes and strict rules for debt collection and accounts payable management will also be crucial in the future. After navigating through the most difficult times, some businesses may benefit from restructuring their debts to more acceptable levels, rebalancing financial distress with profitability. Others may need to secure additional funding to resume certain key investments previously put on hold, or even to proceed with acquisitions that may bring the company to new grounds.

Going forward, strong partnerships may be instrumental for companies to succeed, especially for businesses focusing on local and regional markets. Besides striving to have stronger vertically integrated business partnerships, companies should explore new ways to interact with their customers, financing partners, business partners and regulators.

Figure 1. Strategic framework for addressing COVID-19 impact

Deloitte Dutch Caribbean and its multi-disciplinary teams can support your organization navigating these tough times. Please visit our website https://www.deloitte.com/an/ or reach out using the contact below.